Climate change in the Western Balkans is no longer a distant scenario. It is already a macroeconomic issue that shapes growth, public finances, and EU convergence. Albania, Bosnia and Herzegovina, Kosovo, Montenegro, North Macedonia, and Serbia share a similar story: high exposure to floods, droughts, and heat, aging coal fleets, and institutions still catching up to the pace of change. At the same time, the regional climate transition can unlock tens of billions of euros in resilient infrastructure, clean energy, and new jobs, if policies and investments are sequenced well.

This article summarizes the key findings from recent World Bank Country Climate and Development Reports (ALB, BIH, KOS, MNE, NM, SRB, WB). It highlights the main risks, investment needs, and, importantly, the hidden tensions that are not always spelled out in official documents but matter greatly to policymakers, regulators, investors, and energy professionals.

Climate risks are already macroeconomic in the Western Balkans

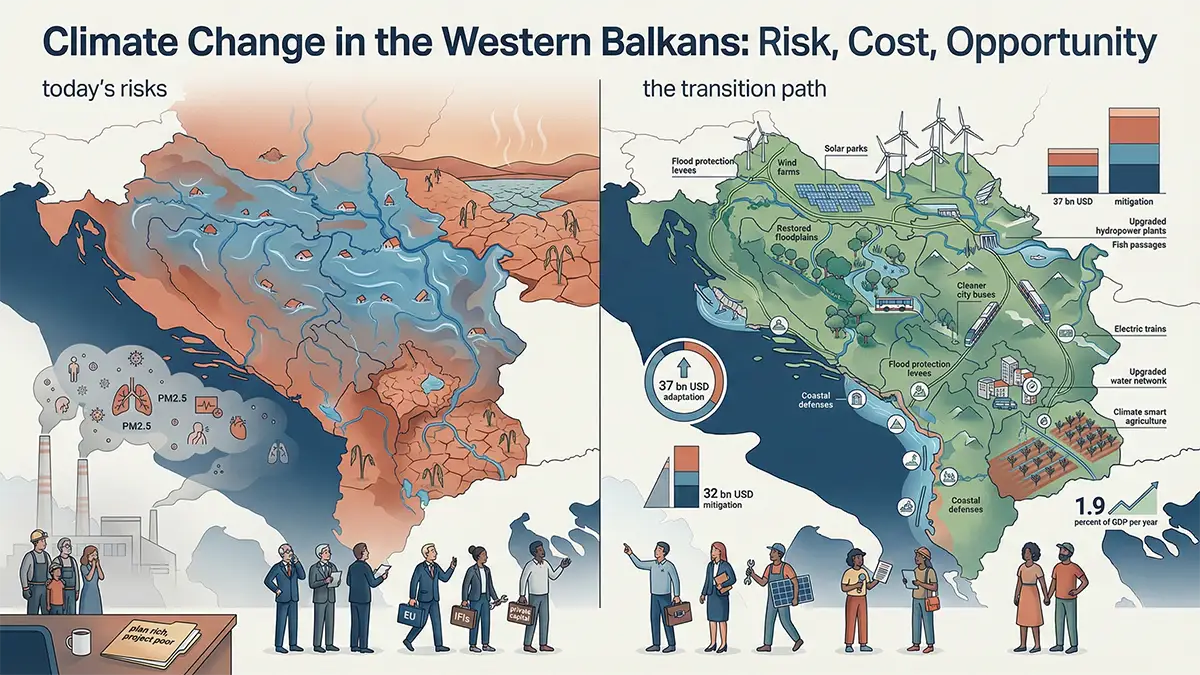

Across the region, physical climate risks are material and rising. Floods are the dominant hazard in several countries. In Bosnia and Herzegovina, floods already account for more than 90 percent of climate-related damages, and without stronger adaptation, gross domestic product (GDP) could be up to 14 percent lower by 2050. Montenegro faces combined risks from floods, landslides, wildfires, and coastal hazards, with climate-related disasters projected to cut GDP by about 7.9 percent by 2050 if adaptation lags. North Macedonia could lose up to 4 percent of GDP, while regional modeling suggests Serbia could see GDP around 15 percent lower by mid-century in a high-impact scenario. These are not just occasional shocks. Droughts and heatwaves threaten agricultural yields, hydropower, and water supply. Cities already face heat stress and local air pollution. High non-revenue water in utilities, aging infrastructure, and informal settlements amplify vulnerability. Climate change acts as a risk multiplier on these existing weaknesses.

Adaptation: from disaster losses to resilience investment

The adaptation agenda in the Western Balkans is extensive, front-loaded, and high-return. The regional CCDR estimates that an initial adaptation package of about 37 billion US dollars will be needed over the next 5 to 10 years, with average adaptation investment needs around 1 percent of GDP per year to mid-century. Each dollar invested is expected to yield roughly four dollars in benefits through avoided damages, higher productivity, and health gains.

Indicative country packages over the next decade are sizeable relative to economic size: about 6.0 billion US dollars for Albania, 6.8 billion for Bosnia and Herzegovina, 2.8 billion for Kosovo, 5.7 billion for Montenegro, 6.4 billion for North Macedonia and 9.5 billion for Serbia. In several countries this corresponds to between 0.6 and more than 2 percent of GDP per year.

The main investment and policy opportunities include:

- Modern flood and drought risk management combines updated hazard maps, climate-resilient river basin plans, and nature-based solutions such as floodplain restoration, peatland protection, and sustainable forest management.

- Upgrading water supply and irrigation systems, especially by cutting non-revenue water toward European Union (EU) benchmarks, which alone implies multi-billion euro investment needs.

- Climate-smart agriculture that improves irrigation efficiency, changes crop choices, and provides risk transfer tools for small farmers.

- Climate resilient infrastructure for transport and energy, supported by modern early warning systems that have benefit-to-cost ratios that can reach hundreds or thousands to one.

- Urban adaptation through resilient land use planning, flood protection in cities, greener public spaces, and housing retrofits that improve both resilience and energy efficiency.

In short, the region has a very concrete pipeline of resilience investments that can reduce disaster losses and strengthen long-term competitiveness.

Mitigation: from lignite lock-in to net zero opportunity

The Western Balkans are not large emitters in absolute terms, but they are highly carbon-intensive per unit of GDP. Power systems in Bosnia and Herzegovina, Kosovo, North Macedonia, and Serbia still rely heavily on lignite coal, with aging and inefficient plants. Buildings are poorly insulated and depend on coal, heavy fuel oil, unsustainable biomass, and inefficient electric heating. Transport remains dominated by old internal combustion vehicles, with weak rail and public transport options. The energy-intensive industry still has limited uptake of best available technologies.

This creates several mitigation risks:

- Exposure to the EU Carbon Border Adjustment Mechanism (CBAM), as carbon-intensive exports face rising implicit carbon costs unless domestic carbon pricing and real decarbonization keep pace.

- Stranded assets, where new or refurbished coal plants, district heating systems, and fossil fuel infrastructure risk becoming uneconomic long before the end of their technical life.

- Persistent air pollution, especially fine particulate matter (PM2.5) from coal and low-quality fuels, which contributes to excess mortality in cities in Bosnia and Herzegovina, North Macedonia, and Serbia.

At the same time, mitigation is a significant opportunity. The regional CCDR shows that the Western Balkans can become climate-neutral by 2050 without sacrificing growth if about 32 billion US dollars in additional mitigation investments are mobilized, focused on power, buildings, transport, and industry. Around 85 percent of this could, in principle, come from private capital, provided that policy and regulatory frameworks improve. Key mitigation opportunities include large scale deployment of solar and wind power using the region’s good resource potential and existing hydropower for flexibility, a managed lignite phase down supported by regional power market integration and grid and storage investments, deep renovation of the building stock combined with heat pumps and cleaner district heating, electrification and better public transport in cities, and industrial decarbonization through efficiency, electrification and, in some niches, green hydrogen.

Climate action as a growth and convergence strategy

The climate agenda is often framed as a cost. The CCDRs take a different view. Taken together, adaptation and mitigation would require average additional investments of around 1.9 percent of regional GDP per year until 2050. This is significant but not out of line with current public investment needs for infrastructure and EU convergence.

The economic case is strong. The adaptation packages mentioned above yield benefit-cost ratios of 2 to 10 when avoided losses, productivity gains, and health improvements are included. The net zero transition is expected to reduce air pollution-related mortality by around 15% by 2050. At the same time, about one in six workers in the region will need to upskill or retrain as the green transition proceeds, creating both pressures and opportunities for better jobs. For investors, the signal is a large, long-term pipeline of green infrastructure, services, and technologies. For governments and regulators, the message is that climate policy is not only about risk management; it is also about steering investment and innovation to support higher productivity, better health, and EU integration.

Key climate risks Western Balkans leaders must watch

Across the six countries, several risk clusters stand out.

First, there are physical and disaster risk hotspots. Flood-prone river basins in Bosnia and Herzegovina and Serbia, flash floods and landslides across mountainous areas, intensifying droughts and heatwaves that hit agriculture and hydropower in Kosovo, North Macedonia, Albania, and Montenegro, growing wildfire risk in forested and coastal areas, and coastal erosion and storm surge in Albania and Montenegro that threaten tourism and infrastructure.

Second, there is energy transition and stranded asset risk. Reliance on lignite in power and heat, delayed investment in grids, storage and flexibility, and abrupt changes in tariffs or support schemes all create uncertainty that can either slow down decarbonization or leave costly assets underused.

Third, fiscal, financial, and CBAM risks are material. High upfront adaptation and mitigation needs, together around 1.9 percent of GDP per year, interact with limited fiscal space and competing social investment priorities. Banks and public utilities carry concentrated exposure to carbon-intensive sectors and climate-exposed assets, which could threaten balance sheets under severe shocks or abrupt policy changes.

Fourth, social and labor risks are significant. Coal-dependent communities and workers in lignite mining and power, as well as in heavy industry, face structural job losses. Energy poverty could worsen if tariff reforms or carbon pricing are implemented without adequate support and efficiency investments for low-income households.

Finally, institutional and governance risks are a recurring theme. Fragmented responsibilities across ministries and agencies, limited climate data, slow permitting and weak enforcement all contribute to a gap between ambitious plans and real project pipelines, leading to a familiar “plan rich, project poor” pattern.

The hidden story: structural tensions in the Western Balkans transition

When the six CCDRs are read together, several underlying contradictions become visible that are not always explicitly stated.

The first tension is between EU-aligned ambition and continued lignite and fossil lock-in. All countries commit on paper to net zero by 2050. At the same time, some plans still envisage operating or refurbishing coal assets well into the 2030s, supported by low regulated electricity prices that make a rapid coal phase-out politically sensitive. The fundamental constraint is not the technical feasibility of renewables but the political economy of coal, tariffs, and social contracts in coal regions.

The second tension is between the expectation that private capital will finance most of the transition and the current weakness of the investment climate. The regional analysis assumes that around 85 percent of mitigation investment will come from private sources. Yet each country report highlights regulatory uncertainty, slow permitting, governance challenges in state-owned enterprises, and shallow capital markets. The implied message is that without rapid institutional reforms, the private share will be lower, and a greater burden will fall on public budgets and international financial institutions.

The third tension is between framing climate action as a growth engine and limited absorptive capacity. The region stands to benefit from substantial climate finance and EU support, but many line ministries, municipalities, and utilities struggle with project preparation and implementation. Feasibility studies, land acquisition, permitting, and procurement often delay or derail projects. In practice, the bottleneck may be administrative capacity rather than the availability of funds.

The fourth tension is between a strong narrative on just transition and relatively modest concrete instruments. All six reports stress the need to protect vulnerable groups and coal communities. However, the described measures are often pilots or high-level concepts rather than fully financed, detailed programs. Without a more robust just transition toolbox, social resistance could slow or block key reforms.

Finally, there is a tension in the sectors presented as climate winners. Tourism and hydropower are repeatedly highlighted as growth opportunities. They are also among the most climate-exposed sectors, facing sea level rise, erosion, heat stress, and changing hydrology. Their success depends directly on the speed and quality of adaptation and sustainable land and water management.

Recognizing these hidden stories is essential for realistic policy design. They explain why technically sound plans often stall and where political and institutional effort must focus.

What policymakers, regulators, and investors should do next

Translating this picture into action means prioritizing a few cross-cutting moves.

First, treat climate risk management as core economic policy, not a side issue. Ministries of finance, economy, and planning need to integrate climate scenarios into macro fiscal frameworks, public investment planning, and debt management.

Second, frontload “no regret” adaptation measures. Early warning systems, flood and drought risk management, water loss reduction, and climate-smart agriculture have strong returns and high social acceptance. Making them visible successes can build credibility for the broader agenda.

Third, accelerate energy sector reforms that unlock private capital while protecting vulnerable consumers. This includes transparent and predictable renewable energy auctions, timely grid reinforcement, modern flexibility tools such as storage and demand response, clear strategies for coal phase-down, and targeted social support and energy efficiency programs for low-income households.

Fourth, invest systematically in institutions and skills. Stronger climate data systems, streamlined permitting, better coordination between central and local governments, and professional project preparation units can sharply increase the rate at which the region turns climate finance offers into real projects. At the same time, active labor-market policies and retraining programs are needed so that one in six workers affected by the transition can move into more productive roles. Fifth, design and fund just transition plans that are specific, territorial, and credible. This means working closely with coal regions on economic diversification, transport and digital connectivity, social services and education, rather than relying only on national-level safety nets.

Climate change will shape the Western Balkans’ development path over the next three decades. Inaction could reduce GDP by up to double-digit percentages in several countries by 2050, undermine social stability, and slow EU convergence. Strategic climate action, by contrast, can deliver resilient infrastructure, cleaner air, better jobs, and a more competitive, integrated regional economy.

The numbers are significant, but they are manageable with the right mix of domestic reforms, EU support, and private investment. The deeper challenge lies in navigating the structural tensions that appear when all six CCDRs are read together: coal politics, weak investment climates, limited administrative capacity, and incomplete just transition instruments. Addressing these head-on, rather than treating them as background noise, is the key to turning climate change from a threat into a driver of modernization in the Western Balkans.

WESTERN BALKANS GHG PROFILE

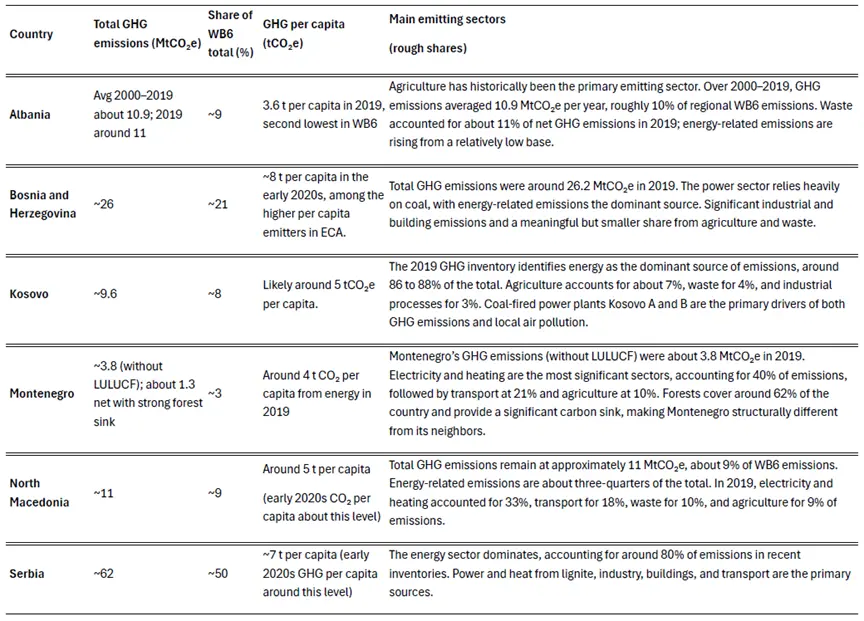

The region’s combined emissions are in the low hundreds of millions of tons of CO₂ equivalent per year, compared with roughly 57 gigatons globally in 2019.

A few common features run through all six countries:

- Energy-related emissions dominate everywhere. In most WB6 economies, around 70–80 percent of GHG emissions come from energy use, especially electricity and heat generation, transport, and fuel combustion in buildings and industry.

- Coal is the key structural problem. Serbia, Bosnia and Herzegovina, Kosovo, and North Macedonia all rely heavily on lignite for power generation, with coal-based electricity the largest single source of emissions.

- Land use, land use change and forestry (LULUCF) is a net sink in some countries, notably Montenegro and parts of the region with high forest cover, which partly offsets energy emissions but does not change the basic coal story.

Table compiled based on the data (Source): CEIC data, UNFCCC, World Bank, Emission Index, The Global Economy, Relief Web, IMF